On March 30, 2010 then President Obama signed a law authorizing the US Department of Education to take over the nation’s student loan issuance. Prior to the law, the federal government issued approximately a third of student loans through its direct-lending program, but as of July 1, 2010 (when the law became effective), banks, schools, and other lenders no longer would issue student loans. The idea was that the government would freeze out predatory lenders, income-driven repayment options would reduce the burden of loan repayment for graduates, and revenue would help fund the Affordable Care Act. While some of that may or may not have come to pass, we have definitely seen the politicization of student loans; and subsidized loans have helped to hide the rising cost of tuition, which, according to the National Center for Education Statistics, has risen from an annual tuition of $8,238 in 1985 to $18,632 by 2015 (dollars are for public four-year institutions and are in constant 2015 dollars), for a compounded increase of 2.87% per year.

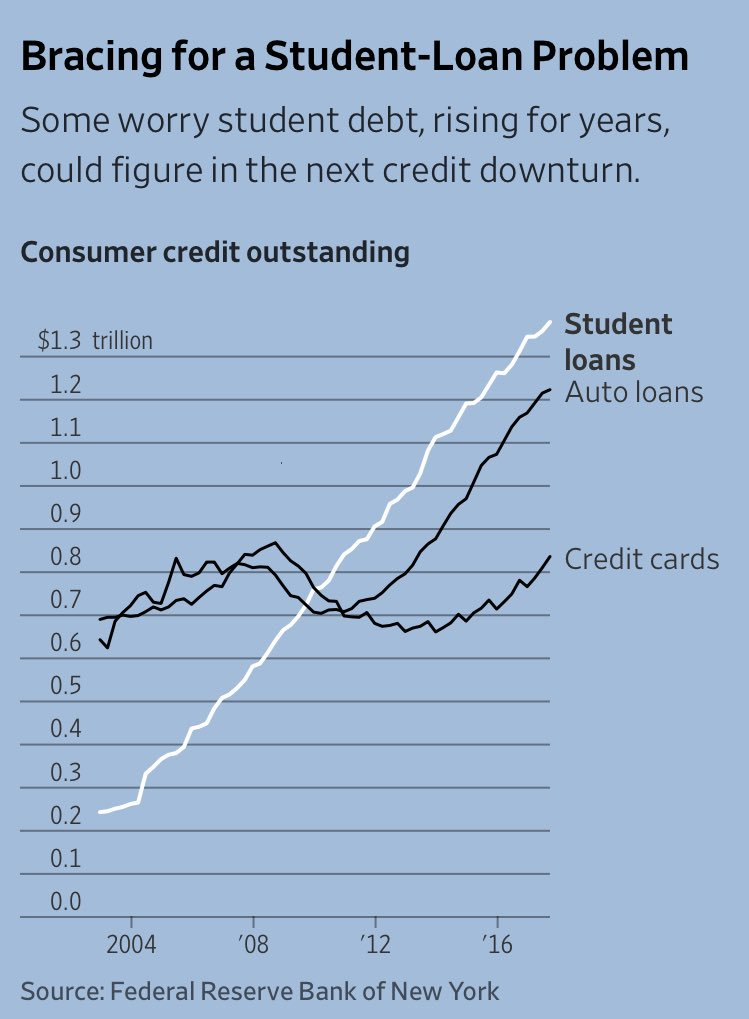

Below is a comparison of student loan debt to auto loan and credit card debt, published by the Federal Reserve Bank of New York. I’m not sure how anyone could see the trend for student loans and not get really concerned. It simply is not sustainable, especially when you consider that, according to The Institute for College Access & Success, 68% of 2015 bachelor’s degree recipients graduated with student loan debt, with the average debt per borrower at $30,100. That is a lot of debt when one considers the lackluster income potential for many majors, that graduate school is necessary for many careers, and that student debt cannot be discharged through bankruptcy.

When I look at that rate of growth in student loan debt, I worry that we are creating serfs of our college graduates, especially since I do not see anything on the horizon that will arrest this trend. It’s scary.

Growing up my family had what was needed, but I do remember being embarrassed that I couldn’t get “cool” clothes and even in junior high I had some hand-me-downs that I hated. I think it instilled a drive to “do better no matter what.” I am in my 50’s and I have been proud that I was able to put myself through school. I was working full time and going to to school full time (and not much socializing). I have come to realize I shouldn’t be comparing what I went through 3 decades ago with the current plight of college students. It is a different world. My dad was the first to ever get a college degree. I got an MBA at night school. All my kids are assuming they will be getting a masters or med school or the like. That isn’t because I am not pushing them. I have told them that being a plumber is good in that your job won’t be offshored.

I am a firm believer in education being great for society, but it is worrisome that (most) colleges have become so expensive. I actually think it, along with a changing job market, is pushing us to where there will be the have’s (college educate) and the have not’s. The bigger that divide, the greater the chance of social unrest. Rising student loan debt is just the outcome of that.

Very expensive here in Britain now too. Tuition fees at £9000 per year, plus further loans for living expenses, mean graduates leave with debt of £50000 minimum for a 3 year bachelors degree, with interest rates over 6% charged from the moment the funds are paid. These are loans from the government, and there are repayment conditions that don’t kick in until a minimum earning, any outstanding to be written off after 30 years, but it effectively makes British graduates indentured servants of the state for most of their working lives. The entire debt can become due for repayment if you decide to go abroad… it worries me hugely.

My opinion on the matter is that for many in the U.S., student loans are simply a lifestyle choice. It’s seemingly easier to take out loans and not have to work (or work only very part time). Many also look down their noses at starting at community college to knock out introductory courses at a small fraction of the cost of a four year university (or attend a less prestigious commuter school) while living at home. Combine that with CLEP testing, and you can knock out 2+ years of college very, very affordably (to say nothing of applying for as many scholarships as possible – it’s shocking how many there are out there and they’re often short on applicants). I’m also a bit biased as I literally went to war to pay for my education (thank you ROTC program), and also parked cars and did office work to cover living expenses.

All that said, I recognize that my thoughts above are very much a middle class opinion. If you’re from a working class family living paycheck to paycheck and/or didn’t have the benefit of a good primary and secondary education, many of the options I mentioned are likely out of reach. Hence the reason I served beside many, many wonderful people who entered the military to qualify for the GI Bill. It’s one of the few pieces of legislation I believe has been a resounding success.

I am also one of those guys that worked my way through college, had scholarships and CLEP’d a lot of hours, but that was in another time. I did take out a loan towards the end because I needed the study time for engineering and couldn’t keep the work going as many hours and get the grades.

One point to about student loans also are that the loan rates are ridiculous. My son got a student loan with an interest rate that was over 6%!! I can buy a car with a cheaper rate than that. My student loans in the 1970’s were at around a percent, and I paid like $75/mo for 10 years to pay it off. If the government wants to encourage education, they should cap the amount of interest that lenders charge. I know it’s not as profitable for the lenders, but something to make education dollars available at a realistic interest rate needs to happen.

Not a cougar; I also paid my own way, but at the end I needed to take out a loan to finish. You can’t compare 30 years ago to today. One quarter of tuition for me in 1978 at a state university was around $500 (or maybe less, I’m getting old) and I was making about $4.50/hr (which was very good back then). Today, my son can only make about $10- 12/hr (unskilled college kid type jobs), but tuition is more like $2,000/semester (and then books, housing and food). Education has more than quadrupled, but minimum wage has barely doubled, so you’re always behind the curve. I have subsidized him some to help him finish, even though he works summers at a good paying job.

I am realizing that I will have to choose between paying for my children’s education or having a comfortable retirement. I am choosing their education, and I intend to die penniless while working at Walmart.

“subsidized loans have helped to hide the rising cost of tuition”

The cynic in me argues this was an unspoken, but primary feature, for proponents backing the US Government takeover of the student loan industry. As my history teacher used to say, “Follow the Money”. There used to be at least a little moral hazard when traditional banking institutions were involved in loan decisions. The moral hazard had a throttling effect limiting the flow of funds to educational institutions. With the Government’s takeover of the student loan industry and very easy qualification requirements, the moral hazard has essentially been eliminated. This was like connecting a school’s financial office directly into the US treasury with the spigot turned wide open.

Interestingly enough, the chart Cody presents shows outstanding loans exceeding the top line number of $1.3 Trillion. If that number sounds familiar, its the same amount of debt the subprime market had in 2007 just as that market tanked.

Paul, it’s been a while since I attended but $2k a semester is a bargain for tuition (go look at what UCLA charges for in-state tuition). Yes, the student is going to need help (e.g., living at home to cut on expenses – which I understand may limit the number of schools the student can reasonably attend), but $2k isn’t a deal breaker, even for someone earning $10 an hour. There are still myriad ways to fund an undergrad education without debt. It may take a bit longer and be far less glamorous, but it can be done; however, it requires sacrificing many of the rites of passage of college life such as living on your own (dorm or apartment), extracurriculars, sports events, Spring Break, etc. Many just aren’t willing to sacrifice those things and turn to debt instead.

Hedgehog: Wow! Those are some eye-watering numbers and it sounds like the UK is in a similar situation to the US in saddling graduates with unsustainable debt. Is there anything afoot there to try and arrest the trend?

Several of you have mentioned the difference between the costs of education years ago and costs today. There is definitely a divergence there, which makes working to pay for school an increasingly difficult proposition. I’d also add that a bachelor’s degree was worth more back then than it is today, with many careers now requiring graduate degrees of some sort in order to be competitive – all of which increases the debt load.

Cody, this is the latest news: http://www.bbc.co.uk/news/education-43810163

There is a review underway, but I am not holding my breath. The interest rates are iniquitous in my view.

Meanwhile my kids are aiming to study engineering (one already in the second year), 4 year MEng courses, which leave little room for outside employment because of time demands for lectures, lab, projects, and which is not especially well paid in this country, if you stay in engineering (a different story if you head for a career in finance).

Furthermore, the university system here is not as flexible as the that in the US.

Dave C: There’s been little moral hazard re: federally backed loans since the 1970s, and virtually none for any kind of student loans (federally-backed or private) since 2005 given laws governing bankruptcy. It’s exceedingly hard to get out from under huge student loan debts and only the federal government as any incentive to engage in income-based repayment options (aka their constituents want options for their loans and their kids’ loans).

Second that Hedgehog. My son”s course demands 1600 hours theory, 1600 hours practice per annum over two years for his masters, so no time for earning. We are financing his living expenses as there were no appropriate courses within travel time, but his fees are his responsibility with an eventual debt of minimum 60 000 sterling. Few scholarships exist.

That debt will then be doubled should he make a life with a graduate. His income is capped within his profession at 50 ooo sterling at present and is unlikely to change above inflation.

How is it possible to serve missions? To pay tithing? Let alone finance a car or home. I’m afraid that the outcome will be a generation without home ownership or indeed pension. A very different financial model for a society with an absence of personal assets.

Wow.

At over a trillion dollars, student loans also represent (by far) the single largest cash receivable of the U.S. Gov. They also provide a higher rate of return (avg. 6.7%) than has otherwise been available. This receivable has essentially already been spent in budget projections for coming years. This makes it politically unlikely that (in spite of much talk) that there will be any meaningful debt forgiveness for student loans.

Student loans are also effectively nondischargeable in bankruptcy, and when you die, your estate remains liable. They are true zombie debt – they never die, they never go away, and they never stop coming for you.

Friend don’t let friends do student loans. They should only be used as a means of last resort, and then only in minimal amount.

We should be concerned and uncomfortable when the federal government, under the stated goal of promoting education, ends up being one of the largest, and certainly the most favored, and thereby onerous, consumer creditor in our country, with the unintended consequence that rather than creating opportunity and prosperity for young adults, rather creates financial despair and servitude for the upcoming generation.

Kevin Anderson — Federal student loans are discharged upon the borrower’s death, not passed on to the estate.

—

I used to work for a student loan company, and at the time I was proud of our stated mission to improve access to higher education. But in hindsight, I’ve wondered if we really did. I think loans not only hide but cause rising tuition. We saw one or two of our less reputable schools hike up their tuition immediately after — and in exactly the same amount as — an increase in the annual limits on how much can be borrowed. I wondered how many schools did the same thing more subtly.

Salaries of campus executives have increased well above the inflation rate, but it feels like a degree is not the golden ticket it used to be. One proposal I read and liked suggested mandatory reporting of the average salaries of each school’s graduates, by major, through cooperation with the IRS. This would give students better data to determine which fields of study are worth the tuition.

I survived the mass layoffs when Obama switched all student loans to Direct, and I was involved in implementing the administration’s other changes. On the homefront, my husband took out Direct loans at the new higher interest rate — 4x what my “pre-Obama” loans had been. But then, my older sister’s loans were also pre-Obama, and market conditions in her day made her interest rate double my husband’s, so I knew it could be worse. I supported the ideals of the ACA, if not necessarily the devils in its details, so I didn’t mind too much. We’ve talked about getting a car loan to pay off these higher interest student loans. It seems like student loans went from a government service to government revenue, but other changes Obama’s administration made (like income-contingent repayment and increased loan forgiveness options) will put a dent in how much gets repaid overall. I don’t know if the interest rate increase and the elimination of middle-man lenders are enough to balance out that dent AND pay for the ACA. The rate increase itself could lead to more defaults. Who bails out the government when these loans default?

You are correct that student loans have contributed to an unnatural increase in college tuition. Since 1978, tuition has increased 1,300%; medical expenses up 700%, while the consumer price index only increased 300%. That’s a 4-times greater increase in tuition other expenses (see dshort.com). Wages have not kept pace with tuition, medical and housing expenses. No wonder reaching a true middle class status has become a rare accomplishment (and then add tithing into the mix).

Another scary statistic is that in 2008 (just before the recession), federal student loan debt was $116 million. It is now $1.1 trillion – that’s almost a ten-fold increase in ten years. And when you add private student loans, the total is $1.45 trillion!

Student loans can be a valuable tool in attaining higher education, but folks need to understand the consequences and very limited debt relief options for such loans.

Laurel – You are correct that under certain circumstances, federal student loans are discharged upon the death of the borrower. Here is a list of when that might not be the case (and note that almost a quarter of student loans are from private lenders):

140011

Private Student Loan – probably not discharged, but only decedent’s estate liable.

Co-Signed Student Loan – not discharged, co-signer remains liable.

Student Loan Incurred While Married – if community property state, then surviving spouse may be liable.

Thanks for your insight Laura. It’s nice to get info from an insider’s point of view 🙂

Kevin Anderson — I am just talking about Federal. By co-signed loans, you might mean a PLUS loan that a parent co-signs for the student, or loans spouses have consolidated into one loan. For the co-signer parent, the loan IS discharged when the student dies (or becomes permanently disabled). Consolidating loans with your spouse is no longer allowed (again, for Federal loans, not private), but for co-signer spouses already in existence, the portion of the loan originally attributable to the deceased /disabled IS discharged. There’s no community property law that would overrule the law that requires discharge of a Federal loan upon death.

Of course, private lenders can do what they want (within legal parameters). But I’m of the opinion that if you can’t pay for school with just Federal loans, you need to take a break from school and flip burgers to save up (what I did), or go to a more reasonably priced community college, or both. I’m sure there are extenuating circumstances that would justify a private loan (parents or other caregivers, foreign students, grad school, etc.), but in general I hold to that smug belief.

I’ve lived in a major FL university town. I saw many student couples/ families in our ward going on trips, purchasing annual Disney passes, owning the lastest mini van , etc. My husband had a very good job and I worked part time and we couldn’t afford those things ( we had 2 teens at he time) . I asked a student how they afforded a weekend Birthday trip to NYC – her answer ‘student loans’. SMH.

Tina, I’ve seen the same thing too…young couples maxing their student loans to have families, drive new minivans, buy new baby car seats (instead of using recalled ones in thrift stores), and occasionally (gasp) going to the movies. They qualify for section 8 housing, Medicaid, and other programs that otherwise, would leave them destitute. Lds women often stay at home with growing little families while husbands pursue MDs, JDs, or MBAs. They live under the poverty line, with just a few perks. In two wards I’ve lived in, there were apartment complexes filled with dozens of such young families.

If it weren’t for these programs and the ability to max student loans, young couples wouldn’t be able to pay for their children and pursue degrees. Period. Don’t let welfare jealousy eat at you. They aren’t living in Trump Tower, cumulatively all these families don’t use a fraction of what is given to the rich through corporate welfare. They will spend the rest of their lives paying back every penny plus interest as well as paying heavy middle-to-upper-class taxes. They will repay “you” (Actually “us”) many times over.

I don’t think the church realizes how impossible their mandates are. Have children. Get and education. Stay out of debt. Go on a senior mission in the next 40 years (while continuing to pay off your student loans, not having homes increase in value as they used to- if you ever get a home, and pay six-figures for each child’s a college tuition). Meanwhile, we are subjected to GA talks that tell us how they (in 1960s) had 10 children in school because they worked a ( “a” meaning “one”) part time job and their high-school educated wife took in laundry. We are expected to do the same- to have large families and not delay childbirth, while functioning in a completely different economic and sociopolitical world. Meanwhile, older members look down at you if you find a foothold in the system that gives you a shred of normality and decency.

I don’t think that we can elevate our nation and communities (not just ourselves) if we subscribe to a black and white view of families as being “makers” or “takers” in an insipid Ayn Rand-hatred of anyone who needs temporary assistance.

Realize it comes back to you. Plant trees whose shade you may not live to enjoy. Your family will have doctors, teachers, scientists, and others in their communities that you otherwise wouldn’t. Children will be born that otherwise wouldn’t. Let go of minivan envy. Minivans aren’t worth envying anyway ; )

Good call Mort. My son hates me nay-saying to the debt, since it’s the world he has to live in. It’s just so hard for them. Time was in the UK that as a child of a loan parent I was able to get a liberal arts degree without debt. That changed my life, my children’s lives and my church service, quite apart from making me a contributing part of society rather than a drain on it.

I was one of those student families on Medicaid and WIC until last year, and I didn’t take Tina’s comment as Ayn Rand hatred. How is describing your experiences hateful? I think it’s relevant to this discussion to point out the contribution of irresponsible borrowing to the debt. It may not be the predominant factor, but it is a thing.

I was grateful for the assistance, and I felt an obligation to be a good steward over what we’d been given. When possible, I bought things second hand — even car seats (you can check if a model has been recalled or expired) — often from other student families. We kept our one car — a 2000 Civic — alive but declined to make cosmetic or convenience repairs. If second hand is such an affront to human dignity, where is the dignity in the consumerism filling landfills with things we could have used if we weren’t so damb dignified? It doesn’t take an ascetic monk to not feel owed a taxpayer-subsidized Disneyland trip or a late-model car. For those who do, fine — so long as they have done the math and know they can comfortably pay the loans back after graduating. But whether they can or can’t, they forfeit their justification to complain about student debt. If I can speak for the rest of us — the ones who use student loans to raise our families and occasionally go to the movies — we’d rather not be lumped with the Disneyland goers by an inference that acknowledging their existence is an assault on all of us.

I agree with Mortimer that student loans are now a fact of life if you want to pursue certain careers. The average med student in the U.S. graduates with about 190k in student loans, and those “average” medical students aren’t supporting dependents on the side. But it’s a career where 95% of the time you’ll be able to pay off the loans sooner or later. I can’t say the same for going into heavy debt for a lot of undergraduate degrees.

Tina, I saw a bit of what you described, but in most cases the extra income was coming from family members. Nothing like seeing a young mom on WIC and Medicaid sporting a $300 diaper bag that was a gift from a family member. If those kids were using student loans for vacations, *someone* was subsidizing their living expenses.

I don’t know how well student loans can compare to home, auto, and other credit loans. The loans aren’t against any physical item that can gain or lose value. No one seems to have any plan to fix the situation either. Complete forgiveness of student loans won’t stop the money flow, and a “crash” is even less likely with the government backing almost every loan. Even if it does crash, what then? Home loans crashed, and it was business as usual.

I didn’t say Tina’s comment specifically was Ayn Rand hatred, but point out that it’s sympotomatic of the Rand cult that so easily judges others. Randism (which I’m railing on more than the people here) creates a sanctimonious “work” ethic based on comparisons and rules someone made up that others are supposed to follow or be labeled and enemy to society. It’s a cocktail of jealousy and and a love of riches above your neighbor.

Who knows how that young couple got a minivan. Maybe they won it in a contest. Maybe they paid for it instead of buying a cheap used car that would cost much more in repairs and put the family in danger. Maybe that $300 purse was purchased second hand. (I just bought a $400 one for $15 the other day. Looks like new. I couldn’t have sewn anything as cheaply.) And what if I had purchased it new, even as a poor person on welfare or student loans? It isn’t our place to judge. Maybe it just. doesn’t. matter. Those of you that have never made a financial mistake, who never splurged, who never gave a “Gift of the Magi” type gift, who have never experienced buyers remorse, who never sacrificed for something that technically one couldn’t afford, can step forward and continue throwing stones. Otherwise, can we agree that maybe it doesn’t matter?

Who made us purse police or Disney park admittance auditors? Sheesh. When that same woman with that purse needs a casserole or lift, are we going to rebuff her? No, we wouldn’t do that, we just money shame her, as is our Godly duty (eye roll).

There was once a poor family that lived in a trailer park. They had no fridge, just a cooler. When the school found out about it, teachers held a fundraiser. People were generous. A huge beautiful stainless steel fridge was purchased that even made ice. Not long after, someone noticed that the family had returned the fridge to the store and used the money to purchase a big tv and gaming system. The community was outraged. They had given the fridge b/c they wanted to solve the food handling need, not waste money on something frivolous.

The family in fact, did not need a fridge. They didn’t even have the plumbing for the ice maker. They had absolutely no room for it, nor did they have the money month-to-month to constantly run it. Their cooler was working fine.

But why buy an expensive tv and gaming system? Because poverty sucks. Because escapism through entertainment and family time provides some normalicy. (Remember how the country loved Hollywood movies during the Great Depression?) Because the trap of poverty is so insidious that even $1000 is just a drop in the bucket. It wouldn’t have gotten them a house, a working car, resolve food insecurity, helped them shift into the middle class, anything really. They knew that the distance between middle-class luxury was several decimal points and an impossible chasm away. They knew that statistically- they had essentially ZERO chance of escaping their poverty, no matter how many “rags to riches” stories or myths there are out there or how much they might piously squirrel away.

The wealth gap and poverty trap are worse than they have been in this country in a very long time. We like to think of the American Dream as being possible, but if you are in the poverty class, you don’t see that dream happen for the people around you.

So not being able to move from a trailer to a home, not being able to escape the whole d$&@! thing, they chose to get something that would provide them with entertainment and escapism, something they could do together as a family. They chose something that would make them smile (not having much that does), something that the kids could use to relate to the other kids at school. They had lived hand to mouth for generations, and appreciated the idea of living for the moment. They knew what was needed most, even if it broke the rules of the sanctimonious Randites. Like President Hinckley knew when donating food to hurricane victims in Central America, candy was dearly needed. He taught us that everyone needs a little something sweet in their lives.

There’s more that I could say and more that has been written on poverty culture. Essentially, their choices are puzzling to others, but are actually rooted in logic and a contextual knowledge we lack. They make a lot of sense,. We might scoff and say, “but I don’t have as nice of a gaming system!” But you have many more nice things, many more releases, and (importantly) the wealth to be able to save for *even* higher priorities. You’ve likely always had a tv, and are taking it for granted. Because you always had one, when you had the chance to upgrade it (which you comfortably do), you didn’t need or want anything big.

My point is, it doesn’t matter whether something is justifiable or not. We can choose to look at our neighbors with jealousy and judgement about their lifestyles and purchases, or look a little deeper and with some compassion. What you discover will be illuminating.

I also reiterate that all the fridges, all the gaming systems, the Disney trips and knock-off purses are infinticimally small compared to corporate welfare and corporate fraud. If you need to run after someone with a pitchfork, stop going after the poor and chase the white collar billion+ dollar criminals in banking, pharma and oil.

Thank you Mortimer! Well stated!

Mortimer makes a valid point here, but I don’t think the post and subsequent comments are being critical of the chronically impoverished, but the affluenza that sometimes occurs among students, Mormon grad students in particular. I used to live in a ward that contained a chiropractic college that brought a new batch of young, married LDS students every year; prior to that, I lived near a university with a dental school that also attracted a disproportionate number of LDS students. In both settings, I observed a common propensity among many (but not all) of these young married students to live a comfortable upper-middle-class lifestyle (luxury apartments, nice cars, vacations, etc.) with no apparent source of income other than loans and various forms of public assistance, as well as Church welfare. They would reproduce beyond their means and have 2 or 3 children before graduating, though I’ve seen as many as 4, usually paid for with Medicaid. Then after they graduate and get established in their careers, they become right-wingers and vote away all the social programs they took advantage of, so future generations can’t use them. It’s practically a trope. My wife and I have often wondered if this “aspirational” grad student lifestyle is being actively promoted to undergrads at BYU (where most of these students originate from). In conversations, my wife frequently heard grad student’s wives talk about the “knock-it-out plan” (having all your kids as early and often as possible while still eligible for Medicaid–yes, it’s a thing).)

Mortimer, I saw no pitchforks. Again, Tina related, with minimal commentary (just three letters!), something she’s observed. Her offending head shake was for the acquaintance who identified her funding source as student loans. A belief that a behavior is irresponsible doesn’t preclude (1) compassion for people with the behavior, (2) allowance that the reasons for individual behavior are not known well enough to be fairly judged, (3) acknowledgment that the people who seem to be engaging in the behavior might actually not be, (4) acknowledgement of my own faults, or (5) recognition of bigger problems.

Jack Hughes,

I too have seen this type of behavior in lds undergrad and grad students. The thing that bothers me most is not their use of social services or even maxed out loans, (which they will repay into the rest of their lives), but the fact that they vote against these programs for others. It’s utter hypocracy.

We can’t keep asking people in our society to postpone having families until their mid-to-late 30’s or 40’s. I don’t begrudge people “reproducing” in their 20’s, even if society blocks them from living wages, health insurance, and pretty much requires them to still be in school. I didn’t close my own health insurance gap until I was about 30 and in my 4th full time job. As I said, if cohorts of young lds families have found a way to get a toe-hold in the system, good for them.

I think the way many LDS families treat young singles and families is horrible. Many young people (especially from big families) are taught to leave the house at 18, and begin fending for themselves. 80/18 is a rule in many families…you have 80 days after your 18th b-day to be out of the house. A high school diploma won’t get you living wages, you can’t work yourself through college anymore, you have to pay for your own car, car insurance, and have no health insurance. Things have changed, this is a completely irresponsible and selfish practice common in our culture.

Keep in mind that while comfortable mid-life parents enter the apex of their earning curve and become empty-nesters, their kids have essentially no choice but to turn to social programs. We tell lds people to turn to family first (which obviously isn’t happening), then government, then lastly the church, while insisting that we pay the church first.

Meanwhile, parents are able to save for their own retirements and senior missions. Younger generations are beginning life under a cloud of debt theirbparents didnt face. Granted, parents can’t pay for tuition these days, for health expenses, etc., but they can let kids live at home when at school and getting started in life. Opening homes to young families ( the pre-nuclear family model) would be another helpful solution. I find it interesting that Republican families are most against these ideas, while at the same time against social programs for young people and families. You can’t have it both ways. Young people and families need support more than ever before.

Laurel,

You may not have pitch forks, but are definitely judging. You could consider being more Christ like.

Mortimer, some of your statements I haven’t found to be true.

“Many young people…are taught to leave the house at 18, and begin fending for themselves…This is a completely irresponsible and selfish practice common in our culture.” At 18 I envied kids on their own! My parents asked me to help them financially by living at home and paying rent (higher than market value) when I turned 18. I stayed until my senior year of college. (For the record, they more than made it up to me when they were in a better position by letting my whole family stay there — rent free this time — for the last bit of my husband’s grad school when it went longer than we’d planned.)

“A high school diploma won’t get you living wages.” It took me a year after graduating college to find a job that wanted my degree. In the meantime, I worked two part-time, not-even-high-school-grad jobs (fast food, housekeeping) to pay for living expenses for my husband and I, plus his part-time community college tuition. We had one car, 10 years old. The only necessity we couldn’t afford was health insurance, but in today’s world that’s not an issue. We couldn’t have sustained any children on that income, but it was enough to support two adults living simply, and I recognized that I was well ahead of many in the world. When my husband finally got a part-time job at Walmart, I felt rich. This was only just over a decade ago.* We define “living” differently if you believe the average childless 18 year old can’t earn a living wage.

*I compared the CPI increase to the min. wage increase between then and now. It’s about the same, with a slightly higher increase in min. wage.

“Parents are able to save for their own retirements and senior missions.” Some are. Some aren’t. I see more of a problem with parents ignoring their retirements in favor of their children’s schooling. From Market Watch: “Based on current trends, we will soon be facing rates of elder poverty unseen since the Great Depression. Of the 18 million workers between ages 55 and 64 in 2012, 4.3 million were projected to be poor or near-poor when they turn 65, including 2.6 million who were part of the middle class before reaching retirement age.”

Here is why a taxpayer might be interested in the lifestyles of student loan recipients:

(1) If we are looking at the aggregate student loan debt increasing over the years, it’s of interest to know how much of the increase is due to an increase in today’s lifestyle expectations. (That’s not to say the disproportionately rising cost of tuition and living and the lower relative value of a degree are not huge factors.) The parents of 2007’s college freshmen had incomes 60% higher than the national average, which is an increase from previous decades. Few kids with claims to poverty culture are attending. They’re much more likely to be the kids of the corporate frauds you mentioned, and unable to scale back their lifestyles for even a little while.

(2) Not everyone will pay it back. In 2017, 11% of new loans default within the first three years. One in six borrowers will default. Additionally, income-contingent repayment and forgiveness options mean even more loans will not be paid back. That means some of these Disneyland trips will be entirely on the shoulders of taxpayers.

(3) It sucks for the student. I know and love one person who regrets how frivolously he borrowed for school. It’s hurting him now.

(4) Probably the least important issue: The principle of it. One time a friend subbed for me at work so I could study for a test, even though she had to study, too. I went home and watched TV instead. It was rotten of me. My friend was working whether I studied or not, but using my free time for a purpose other than her gift of time was given was wrong. Older me understands why I did it — the flesh was weak; I just couldn’t stand studying. But it was still wrong. I also can’t stand when tithing funds are used for frivolous things. People sacrificed for the church to have those funds. Taxes are a burden for many people. If you are going to bring up compassion, where is the compassion for them? Ask the people at the bottom of the tax brackets if it’s okay if a student who lives (and will always live) better than they do can borrow money for a vacation.

I consider myself a moderate Democrat. I believe there should be safety nets. I defend against Republicans who believe that Democrats think everything is an entitlement. I’m being proved wrong. I can’t believe we’re even having a discussion about whether taxpayers should pay for Disneyland.

JR in AR — Of course I’m judging. So is Mortimer (Tina is envious, parents of independent 18YOs are selfish and irresponsible, etc.). So are you (Laurel is unChristlike). It is impossible to have an opinion about what is right and wrong (or just worthy of a head shake) without forming some sort of a judgment. I don’t believe God’s directive to judge not was an admonition to abandon all efforts to discern between right and wrong.

Know what else I think is wrong? Racial discrimination. Bank robbery. Corporate greed. Popping gum loudly in public. That doesn’t mean I think the people who engage in these behaviors are terrible or more sinful than me, or forget that there, but for the grace of God, I could have gone in different circumstances.

You don’t get non-judgmental points for not judging something you didn’t think was wrong in the first place. For example, I don’t see anything wrong with wearing the color red. Therefore, I don’t judge people in red, even though some ultra-Orthodox Jews do, That hardly qualifies me as non-judgmental. On the other hand, I think yelling at your kids is wrong, but when I hear a screaming mom my heart (usually) goes out to her (and her kids) because I get that mom days are long, tempers are short, and kids are kids. That is probably as close as I come to being non-judgmental.

Opining on right vs. wrong is kind of what we do on this blog. We pick apart words of general authorities and decide what they should and shouldn’t have said. We get indignant when conservatives go against our progressive moral compass. We criticize bishops for not recognizing abuse for what it is, and the abusers for abusing. The first judgment stone was cast a long time ago. Ours are all in the pile. So let’s all consider being more Christlike, and then discuss our opinions on their own merits, without character attacks.

Not sure how my comment disappeared. Here it is again, more or less:

JR in AR:

Of course I’m judging. So is Mortimer (Tina is envious, parents are selfish and irresponsible, etc). So are you (Laurel is unChristlike). The only difference is the behavior we are judging. It’s impossible to have an opinion about what is right and wrong (or just worth a head shake) without making some sort of judgment. I don’t think God’s “judge not” directive meant to completely abstain from discerning right from wrong. By that definition, a belief that judging is wrong is a judgment, and therefore wrong.

Know what else I think is wrong? Racial discrimination. Bank robbery. Corporate greed. Popping gum loudly in public. That doesn’t mean I think people who engage in these behaviors are terrible or more sinful than me. I know that, but for the grace of God, there I could go in different circumstances. It DOES mean I hold opinions about how people should treat each other.

I don’t get non-judgmental points for not judging something I didn’t think was wrong in the first place. For example, I don’t judge people wearing red, because I don’t think it’s wrong — even if some ultra-Orthodox Jews do. That doesn’t make me non-judgmental. On the other hand, I think yelling at your kids is wrong. But when I hear a screaming mom, my heart (usually) goes out to her (and her kids), because I know mom days are long, tempers are short, and kids are kids. That’s as close to non-judgmental as I get.

Besides, opining on right vs. wrong is kind of what we do on this blog. We pick apart words of General Authorities and decide what they should and shouldn’t have said. We get indignant over conservatives violating our progressive moral compasses. We criticize bishops for not recognizing abuse, and abusers for abusing. If a personal interpretation of the Golden Rule is stone-casting, the first stone was thrown a long time ago. Our stones are all in the pile. So let’s all consider being more Christlike, then continue discussing the relative merits of our opinions, without character attacks.

I’m not meaning to get the last word, but just wanted to point out a few things.

-People can default on student loans for a time, but not indefinitely. Even bankruptcy cannot erase them. You will have to return back to them, and the penalties. Death is the only escape, and sometimes debt is shouldered by widows/widowers if one structures it that way.

– Student loan forgiveness programs are not magic wands. Ususally it’s tit for tat. I worked for the government for 10 years in a job that enabled me to enroll in a program, sacrificing working for higher wages in indistry. For me, it was a wash- a way for the government to pay comparative wages. These programs attract STEM teachers, docs to needy rural areas (sorta like that old tv show “Northern Exposure”), teachers to poor areas, people to careers that are desperately needed, etc. it’s freakin’ hard work- usually for 10 years. It’s NOT like Oprah saying “you get a free loan! And You get a free loan! And you get a free loan!” Nope. It’s really hard work.

-I know there are different ways parents deal with 18 year olds, but speaking generally, lds jello belt culture expects young adults to get out of the nest at 18.

– I agree, the crisis in higher ed costs, health insurance, etc are causing new dilemmas. Just pointing out that there are many fairly wealthy parents who continue into comfortable missions/retirements/ travel while brushing off children’s young adult needs. Just saying.

-I agree that people can be uncompassionate with resources. (Your tv story was poignant). But, when we start getting tied in knots worrying about whether others are misusing resources which we resent having to pay into, we’re in the jealousy zone- the “this Is why the United Order failed” zone, the “oh my gosh, that cheap woman- she skimmped on a full cup of cream!” Zone. At the end of that excellent story (which I’ll reuse, thank you), the temporal things don’t end up evenly, but think about the spiritual/long term effects. She got warm fuzzies for being generous and doing a good deed. The tv watcher felt something g like guilt or unkindness. Think about the big take-always, it begins to be less unfair.

If I can quote the illustrious Oprah again, “you do you.” Yes, a good formula… “you just worry about doing you”.

It really doesn’t matter. It comes out in the wash. Most programs are set up to help a lot of people, and there are amazing people who put in safety rails. Yes, there will always be cheats and frauds, and we can work to stop that, but for the most part, the good outweighs the exceptions.

I probably do mean to get the last word. My husband tells me it’s a habit of mine.

So, default. A few points:

*Federal student loans ARE discharged in bankruptcy when repaying them proves to be an “undue hardship.” 40% of petitions for student loan bankruptcy discharge are successful. (In your defense, only 1% of bankruptcy-filing student borrowers try, probably because of misconceptions about student loans and bankruptcy.)

*Federal student loans are NEVER passed on to the surviving spouse. The only way a spouse could get stuck with the debt is if they take out a private loan to pay off the student loan (at which time, it’s no longer a Federal loan). Is that what you mean by “if one structures it that way”? Even then, it’s easier to discharge a non-student-loan in bankruptcy.

*Good point about the temporary nature of defaults. I had to look into that. Apparently, the statistic is that half of what happens in default stays in default.*

As for forgiveness, it sounds like you did a Public Service forgiveness. I agree it’s a sham. (Common ground! Yay!) I feel compelled to say thank you for your service, whatever it was, because the best thing you can say about that program is it takes the edge off the pain of rejecting the higher salaries in the private sector for some altruistic people.

But what I was thinking of were the new (as in, first-term Obama) repayment plans that base payments solely on discretionary (meaning in excess of 150% of the poverty line) income, and whatever balance remains after 10 years is written off. I agree with these programs, but they do mean that not all funds borrowed will be repaid.

I’m not willing to call it jealousy. I dislike how much of my taxes go to military spending, but I’m certainly not jealous of soldiers and high-tech missiles. I would just prefer it was redirected to people who needed it. And was that a reference to milk strippings? Because this mama bear would’ve un-Friended Sister Marsh so fast if she’ was taking cups of cream from my babies’ mouths to pay for a birthday trip to NYC. “Cheap” is the nicest thing I’d call her.

Have you ever read Oscar Wilde’s “The Devoted Friend”? The well-off antagonist is constantly taking advantage of his poor friend and congratulating himself on his kindness in giving him the opportunity to serve him. I feel like viewing my “TV story” in a positive light would make me too much like the antagonist.

To be clear, I’m not knocking student loans. I think the Federal program has more protections from abuse than most social programs. I’ll restate that I think it’s contributed to the excessive increase in tuition by, as the OP said, hiding costs, but I think on the whole it’s good for individuals and society.

*https://www.americanprogress.org/issues/education-postsecondary/reports/2017/12/14/444011/student-loan-defaulters/

Laurel, I’m assuming that if people are maxing out student loans, they are taking both private and fed loans. Many MD, JD, and grad programs necessitate taking out both private and federal loans just to pay tuition. Private loans can be consolidated with a spouse as a joint debt. Upon the death of one, the other (in that circumstance) is responsible for repayment. Fin aid offices will beg you not to do this, even though the restructure can reduce monthly payments.

I don’t have a burning desire to dive into the minutia of student-loan-land, but I highly doubt that the formulas for writing off student loan debt would allow an MD to declare bankruptcy upon graduation and then write off six figures of student debt for the rest of his/her life while earning gobs of money. If that were true, I know a whole slew of MBAs, PhDs, JDs,MDs, etc, who would be pulling that off. It makes sense that smaller loans to persons with less earning ability, or drastic life events (disability, hardship, etc.) probably figure into those calculations. I’m ok with that.

I don’t t think public service forgiveness programs are a sham, i think they were a good idea. The GI Bill is similar in many ways. Many loan programs have been hacked away at by politicians who didn’t believe in them or felt they were sapping “their” money. Currently, the biggest programs are unrecognizable.

Yup, I was referring to the Marsh story. It wasn’t as we were taught in Sunday School. She was malaigned. The knee-jerk reaction and the jealousy of neighbors (coupled with some other contextual things involving both she and her husband and their pacifistic pushback against some of the retaliatory strikes during the Mormon War) caused the saints to bully and vilify her for generations. In the end, they nit-picked her small (immeasurable) cream contributions. I personally think she was targeted over something so mind-numbingly petty because she didn’t have any chinks in her character.

That protective reaction – that jealousy – betrayed one of the truly great families of early Mormonism. The lesson we to this day have failed to learn is the one President Monson taught- “never let a problem to be solved become more important than a person to be loved.”

I’m not just being gushy- I’m saying that our judgements and initial feelings are wrong when trying to address these problems. When feelings become anger, jealousy, annoyance, or protectionism, we enter a zero-sum game- a “me vs you” scenario where someone is a taker and someone a loser. When we try to ensure that all families have the resources to study and work and access aid where needed, we need to be in a “win-win” frame of mind that puts families and persons above things.

Lastly, I think the tv story is good because it teaches people to look at how their need impacts a neighbor and consider not just what is good for the self, but for the other. No fingers pointed anywhere. Next time you tell it say, “I have a friend ..”

Peace out! (Signing off)

I thought I could resist responding, but my husband’s right. Just three points and I’ll try really, really hard to stop:

I agree Sister Marsh has been much maligned in Sunday schools around the world, but I was operating with OJ’s “if she did it” and adding a hypothetical motive. I imagine a cup of cream was a bigger deal back then.

About forgiveness, I agree it won’t benefit the really high earners. But it will benefit many. For example, a Mormon-sized family of 5 with a decent income of $100,000 who took out the maximum allowable Stafford loans (no Grad PLUS because I don’t want to work through amortization with multiple interest rates) for three years, half ($34,000) of their total debt ($61,500) would be written off.

Your conclusion — “We need to be in a ‘win-win’ frame of mind that puts families and persons above things” — is kind of what I’m saying. I’m against the materialism that leads to misuse of the tax contributions of families and persons who’ll never have the opportunity to be as materialistic.

I learned about the severity of this problem the hard way. $170k in debt and graduated with no job! Thankfully I’ve been able to manage very well, but we all need to do a better job of preparing these students for making a very, very important financial decision.